Latest Tax Rules in Thailand 2025: An Academic Analysis of Tax Structures, Legal Compliance, and the Role of Language Professionals in an International Context

Author: Phakaporn Tanjararak

April 29, 2026, Bangkok – This academic article aims to analyze the latest tax regulations in Thailand in 2025, focusing on the structure of personal income tax, foreign-sourced income taxation, and corporate taxation, as well as lawful approaches to reducing tax burdens. In addition, the article emphasizes the role of certified translators, translation certification providers, and certified interpreters, particularly within the context of the Southeast Asian Association of Translators and Interpreters, in supporting the accuracy of cross-linguistic tax documentation. The findings indicate that a systematic understanding of tax law, combined with support from both legal and language professionals, is a key factor in reducing risks and enhancing compliance efficiency (Revenue Department, 2025).

Introduction

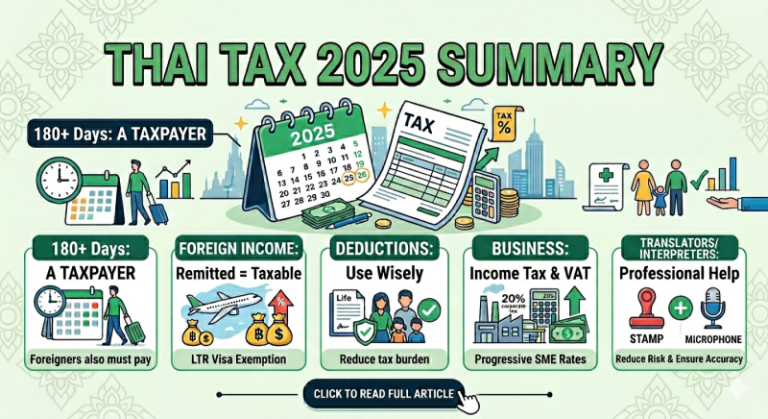

As Thailand’s tax season approaches, the government has strengthened its tax regulations to align more closely with international standards. Individuals who are required to pay taxes, such as those employed by Thai companies or earning income from property rentals, must comply with these tax guidelines or risk legal consequences. Any individual who resides in Thailand for at least 180 days within a calendar year, whether consecutively or not, is classified as a “tax resident” and must file a personal income tax return (Revenue Department, 2025).

This requirement also applies to expatriates, who are liable for taxation if their assessable income meets the required threshold, with exemptions granted only in limited circumstances. Although the tax filing deadline falls in March of the following year, understanding the 2025 tax regulations is essential to avoid costly issues with the Revenue Department.

Analysis of Personal Income Tax Structure

All tax residents in Thailand are required to file an income tax return, although only those whose income exceeds a minimum threshold are required to pay personal income tax. Thailand employs a progressive tax system, with rates ranging from 5% to 35%. As net income increases, the applicable tax rate rises accordingly (Revenue Department, 2025).

However, each tax rate applies only to the portion of income within that bracket, not to the total income. The tax brackets range from income above 150,000 baht to more than 5,000,000 baht, with increasing rates applied progressively. The first 150,000 baht of net income is exempt from taxation, although filing is still required.

Taxation of Foreign-Sourced Income

Thailand’s tax regulations apply not only to domestically earned income but also to foreign-sourced income that is remitted into the country. Tax residents are required to pay taxes on such income regardless of when it was earned, except in specific cases such as individuals holding a Long-Term Resident visa (Revenue Department, 2025).

A proposed amendment to the taxation of foreign income is currently under consideration. If implemented, certain types of foreign income may be eligible for tax exemption, provided that the income is remitted to Thailand within 12 months of the calendar year in which it was generated.

Corporate Taxation in Thailand

Businesses operating in Thailand, whether owned by Thai nationals or foreigners, are required to pay various forms of corporate tax. The primary corporate tax is typically levied at a rate of 20% on net profits. However, small and medium-sized enterprises may benefit from lower progressive tax rates (Department of Business Development, 2025).

Additionally, businesses with annual revenue exceeding 1.8 million baht must register for Value-Added Tax (VAT), which is imposed on goods and services at each stage of production or distribution. Although VAT is ultimately borne by consumers, businesses are responsible for collecting and remitting the tax to the Revenue Department.

Lawful Tax Reduction Strategies

Taxpayers may reduce their tax burden through allowable deductions and allowances, including personal allowances, spousal allowances, child allowances, life insurance premiums, social security contributions, and provident fund contributions. These mechanisms reduce taxable income and may result in a lower tax bracket (Revenue Department, 2025).

Another method involves verifying whether a Double Taxation Agreement exists between Thailand and the taxpayer’s home country. Such agreements prevent double taxation on foreign income. Thailand currently maintains such agreements with more than 60 countries.

Discussion

The findings indicate that compliance with Thailand’s tax regulations is complex both structurally and practically, particularly for foreign taxpayers who face language barriers and differences in legal systems. Certified translators, translation certification providers, and certified interpreters, recognized by the Southeast Asian Association of Translators and Interpreters, therefore play a crucial role in ensuring the accurate translation of tax documents, financial agreements, and legal materials in accordance with government requirements.

These language professionals not only convey meaning but also reduce misinterpretation of legal information, which could otherwise lead to errors in tax filing or non-compliance. Furthermore, they contribute to certifying document accuracy for official procedures and international transactions, thereby enhancing credibility and transparency within the tax system (Southeast Asian Association of Translators and Interpreters, 2024).

The Role of Legal and Tax Consultants

Seeking advice from tax professionals, such as tax lawyers, enables taxpayers to better understand complex regulations and comply effectively. This is particularly important in areas such as tax planning, benefit utilization, and financial documentation management. Professional guidance helps minimize errors and improve procedural efficiency (Siam Legal International, 2025).

Conclusion

Thailand’s tax regulations in 2025 are complex and increasingly aligned with international standards. Understanding tax structures and properly utilizing available benefits are essential for reducing tax burdens and avoiding legal issues. Moreover, support from both legal and language professionals, particularly certified translators and interpreters, plays a significant role in promoting accuracy, transparency, and efficiency in tax compliance within an international context.

References

- Department of Business Development. (2025). Business operations and corporate tax guidelines.

- Revenue Department. (2025). Personal income tax regulations and compliance guidelines.

- Siam Legal International. (2025). Legal and tax consultancy services for foreigners in Thailand.

For professional services, please visit: https://www.seaproti.org/practitioners/

About certified translators, translation certifiers, and certified interpreters associated with SEAProTI. The Southeast Asian Association of Professional Translators and Interpreters (SEAProTI) has officially shared the qualifications and requirements for becoming Certified Translators, Translation Certification Providers, and Certified Interpreters in Sections 9 and 10 of the Royal Gazette, which was published by the Prime Minister’s Office in Thailand on July 25, 2024. Certified Translators, Translation Certification Providers, and Certified Interpreters

The Council of State has proposed the enactment of a Royal Decree, granting registered translators and recognised translation certifiers from professional associations or accredited language institutions the authority to provide legally valid translation certification (Letter to SEAProTI dated April 28, 2025)

SEAProTI is the first professional association in Thailand and Southeast Asia to implement a comprehensive certification system for translators, certifiers, and interpreters.

Head Office: Baan Ratchakru Building, No. 33, Room 402, Soi Phahonyothin 5, Phahonyothin Road, Phaya Thai District, Bangkok 10400, Thailand

Email: hello@seaproti.com | Tel.: (+66) 2-114-3128 (Office hours: Mon–Fri, 09:00–17:00).

กฎระเบียบภาษีล่าสุดในประเทศไทย พ.ศ. 2568: การวิเคราะห์เชิงวิชาการเกี่ยวกับโครงสร้างภาษี การปฏิบัติตามกฎหมาย และบทบาทของผู้เชี่ยวชาญด้านภาษาในบริบทสากล

ผู้เขียน: ภคพร ตันจรารักษ์

29 เมษายน 2569 – บทความวิชาการนี้มีวัตถุประสงค์เพื่อวิเคราะห์กฎระเบียบภาษีล่าสุดของประเทศไทยในปี พ.ศ. 2568 โดยมุ่งเน้นการอธิบายโครงสร้างภาษีเงินได้บุคคลธรรมดา ภาษีเงินได้จากต่างประเทศ และภาษีนิติบุคคล รวมถึงแนวทางในการลดภาระภาษีอย่างถูกต้องตามกฎหมาย นอกจากนี้ บทความยังให้ความสำคัญกับบทบาทของนักแปลรับรอง ผู้ให้การรับรองการแปล และล่ามรับรอง โดยเฉพาะในบริบทของสมาคมวิชาชีพนักแปลและล่ามแห่งเอเชียตะวันออกเฉียงใต้ ซึ่งมีส่วนสำคัญในการสนับสนุนความถูกต้องของเอกสารทางภาษีข้ามภาษา ผลการวิเคราะห์ชี้ให้เห็นว่าความเข้าใจเชิงระบบเกี่ยวกับกฎหมายภาษีควบคู่กับการสนับสนุนจากผู้เชี่ยวชาญทั้งด้านกฎหมายและภาษา เป็นปัจจัยสำคัญในการลดความเสี่ยงและเพิ่มประสิทธิภาพในการปฏิบัติตามกฎหมาย (กรมสรรพากร, 2568)

บทนำ

เมื่อฤดูกาลยื่นภาษีของประเทศไทยใกล้เข้ามา รัฐบาลได้ปรับปรุงกฎระเบียบด้านภาษีให้สอดคล้องกับมาตรฐานสากลมากยิ่งขึ้น บุคคลที่มีหน้าที่เสียภาษี เช่น ผู้ที่ทำงานในบริษัทไทยหรือมีรายได้จากการให้เช่าทรัพย์สิน จำเป็นต้องปฏิบัติตามแนวทางภาษีดังกล่าว มิฉะนั้นอาจเผชิญผลทางกฎหมาย บุคคลที่พำนักอยู่ในประเทศไทยไม่น้อยกว่า 180 วันภายในหนึ่งปีปฏิทิน ไม่ว่าจะต่อเนื่องหรือไม่ จะถูกจัดประเภทเป็น “ผู้มีถิ่นที่อยู่ทางภาษี” และต้องยื่นแบบแสดงรายการภาษีเงินได้ (กรมสรรพากร, 2568)

ข้อกำหนดนี้ครอบคลุมถึงชาวต่างชาติซึ่งมีหน้าที่เสียภาษีหากมีรายได้พึงประเมินถึงเกณฑ์ที่กำหนด โดยข้อยกเว้นมีเพียงในบางกรณีเท่านั้น แม้ว่ากำหนดเวลายื่นแบบภาษีจะอยู่ในเดือนมีนาคมของปีถัดไป แต่การทำความเข้าใจกฎระเบียบภาษีในปี พ.ศ. 2568 ถือเป็นสิ่งจำเป็นเพื่อหลีกเลี่ยงปัญหาที่อาจก่อให้เกิดค่าใช้จ่ายสูงกับกรมสรรพากร

การวิเคราะห์โครงสร้างภาษีเงินได้บุคคลธรรมดา

ผู้มีถิ่นที่อยู่ทางภาษีในประเทศไทยทุกคนมีหน้าที่ยื่นแบบแสดงรายการภาษีเงินได้ แม้ว่าจะมีเพียงผู้ที่มีรายได้ถึงเกณฑ์ขั้นต่ำเท่านั้นที่ต้องชำระภาษี ระบบภาษีเงินได้บุคคลธรรมดาของประเทศไทยเป็นระบบอัตราก้าวหน้า โดยมีอัตราภาษีตั้งแต่ร้อยละ 5 ถึงร้อยละ 35 กล่าวคือ ยิ่งรายได้สุทธิเพิ่มขึ้น อัตราภาษีที่ต้องชำระก็จะสูงขึ้นตามลำดับ (กรมสรรพากร, 2568)

อย่างไรก็ตาม อัตราภาษีในแต่ละช่วงจะคำนวณเฉพาะรายได้ในช่วงนั้น ไม่ได้คำนวณจากรายได้รวมทั้งหมด โดยโครงสร้างอัตราภาษีประกอบด้วยช่วงรายได้ตั้งแต่ 150,001 บาทขึ้นไปจนถึงมากกว่า 5,000,000 บาท ซึ่งมีอัตราภาษีเพิ่มขึ้นตามลำดับ ทั้งนี้ รายได้สุทธิในช่วง 150,000 บาทแรกได้รับการยกเว้นภาษี แต่ยังคงมีหน้าที่ยื่นแบบแสดงรายการ

ภาษีเงินได้จากต่างประเทศ

กฎหมายภาษีของประเทศไทยไม่ได้จำกัดเฉพาะรายได้ที่เกิดขึ้นภายในประเทศเท่านั้น แต่ยังครอบคลุมถึงรายได้จากต่างประเทศที่ถูกนำเข้ามาในประเทศ โดยผู้มีถิ่นที่อยู่ทางภาษีต้องชำระภาษีจากรายได้ดังกล่าวไม่ว่ารายได้นั้นจะเกิดขึ้นเมื่อใด ยกเว้นในกรณีที่เข้าเงื่อนไขเฉพาะ เช่น ผู้ที่ได้รับวีซ่าผู้พำนักระยะยาว (Long-Term Resident) (กรมสรรพากร, 2568)

ทั้งนี้ มีข้อเสนอในการปรับปรุงกฎเกณฑ์เกี่ยวกับการจัดเก็บภาษีจากรายได้ต่างประเทศ โดยหากมีการประกาศใช้ ผู้มีรายได้บางประเภทอาจได้รับการยกเว้นภาษี ภายใต้เงื่อนไขว่ารายได้นั้นถูกนำเข้ามาในประเทศไทยภายใน 12 เดือนนับจากปีภาษีที่เกิดรายได้

ภาษีนิติบุคคลในประเทศไทย

ธุรกิจในประเทศไทยไม่ว่าจะเป็นของคนไทยหรือชาวต่างชาติ มีหน้าที่ต้องชำระภาษีนิติบุคคลหลายประเภท โดยภาษีหลักที่ใช้กับธุรกิจส่วนใหญ่คือภาษีเงินได้นิติบุคคลในอัตราประมาณร้อยละ 20 ของกำไรสุทธิ อย่างไรก็ตาม ธุรกิจขนาดกลางและขนาดย่อมอาจได้รับอัตราภาษีแบบก้าวหน้าที่ต่ำกว่า (กรมพัฒนาธุรกิจการค้า, 2568)

นอกจากนี้ หากธุรกิจมีรายได้เกิน 1.8 ล้านบาทต่อปี จะต้องจดทะเบียนภาษีมูลค่าเพิ่ม ซึ่งเป็นภาษีที่เรียกเก็บจากสินค้าและบริการในแต่ละขั้นตอนของการผลิตหรือจำหน่าย แม้ว่าภาษีดังกล่าวจะเป็นภาระของผู้บริโภค แต่ผู้ประกอบการมีหน้าที่จัดเก็บและนำส่งให้แก่กรมสรรพากร

แนวทางการลดภาระภาษีอย่างถูกต้องตามกฎหมาย

ผู้เสียภาษีสามารถลดภาระภาษีได้ผ่านการใช้สิทธิหักลดหย่อน เช่น ค่าลดหย่อนส่วนบุคคล คู่สมรส บุตร เบี้ยประกันชีวิต เงินสมทบประกันสังคม และเงินสะสมกองทุนสำรองเลี้ยงชีพ ซึ่งช่วยลดรายได้ที่ต้องเสียภาษีและอาจทำให้อยู่ในอัตราภาษีที่ต่ำลง (กรมสรรพากร, 2568)

อีกแนวทางหนึ่งคือการตรวจสอบข้อตกลงการเว้นการเก็บภาษีซ้อนระหว่างประเทศไทยกับประเทศอื่น ซึ่งช่วยป้องกันการเสียภาษีซ้ำซ้อนในรายได้จากต่างประเทศ ปัจจุบันประเทศไทยมีข้อตกลงดังกล่าวกับมากกว่า 60 ประเทศ

อภิปรายผล

ผลการวิเคราะห์ชี้ให้เห็นว่าการปฏิบัติตามกฎหมายภาษีในประเทศไทยมีความซับซ้อนทั้งในเชิงโครงสร้างและเชิงปฏิบัติ โดยเฉพาะในกรณีของผู้เสียภาษีชาวต่างชาติที่ต้องเผชิญกับอุปสรรคด้านภาษาและความแตกต่างของระบบกฎหมาย การมีนักแปลรับรอง ผู้ให้การรับรองการแปล และล่ามรับรอง ซึ่งได้รับการยอมรับจากสมาคมวิชาชีพนักแปลและล่ามแห่งเอเชียตะวันออกเฉียงใต้ จึงมีบทบาทสำคัญในการแปลเอกสารภาษี สัญญาทางการเงิน และเอกสารทางกฎหมายให้มีความถูกต้องและสอดคล้องกับข้อกำหนดของหน่วยงานรัฐ

ผู้เชี่ยวชาญด้านภาษาดังกล่าวไม่เพียงแต่ทำหน้าที่ถ่ายทอดความหมาย แต่ยังช่วยลดความคลาดเคลื่อนในการตีความข้อมูลทางกฎหมาย ซึ่งอาจนำไปสู่ความผิดพลาดในการยื่นภาษีหรือการปฏิบัติตามกฎหมาย นอกจากนี้ ยังมีบทบาทในการรับรองความถูกต้องของเอกสารเพื่อใช้ในกระบวนการทางราชการและธุรกรรมระหว่างประเทศ อันเป็นการเสริมสร้างความน่าเชื่อถือและความโปร่งใสในระบบภาษี (สมาคมนักแปลและล่ามแห่งเอเชียตะวันออกเฉียงใต้, 2567)

บทบาทของที่ปรึกษากฎหมายและภาษี

การขอคำปรึกษาจากผู้เชี่ยวชาญด้านภาษี เช่น นักกฎหมายภาษี สามารถช่วยให้ผู้เสียภาษีเข้าใจข้อกำหนดที่ซับซ้อนและปฏิบัติตามได้อย่างถูกต้อง โดยเฉพาะในกรณีที่เกี่ยวข้องกับการวางแผนภาษี การใช้สิทธิประโยชน์ และการจัดการเอกสารทางการเงิน ผู้เชี่ยวชาญสามารถช่วยลดความเสี่ยงจากความผิดพลาดและเพิ่มประสิทธิภาพในการดำเนินการ (สยาม ลีเกิล อินเตอร์เนชันแนล, 2568)

สรุป

กฎระเบียบภาษีของประเทศไทยในปี พ.ศ. 2568 มีความซับซ้อนและมีการปรับปรุงให้สอดคล้องกับมาตรฐานสากล การทำความเข้าใจโครงสร้างภาษีและการใช้สิทธิประโยชน์อย่างถูกต้องเป็นปัจจัยสำคัญในการลดภาระภาษีและหลีกเลี่ยงปัญหาทางกฎหมาย นอกจากนี้ การสนับสนุนจากผู้เชี่ยวชาญทั้งด้านกฎหมายและภาษา โดยเฉพาะนักแปลและล่ามที่ได้รับการรับรอง มีบทบาทสำคัญในการส่งเสริมความถูกต้อง ความโปร่งใส และประสิทธิภาพในการปฏิบัติตามกฎหมายภาษีในบริบทระหว่างประเทศ

เอกสารอ้างอิง

- กรมพัฒนาธุรกิจการค้า. (2568). แนวทางการดำเนินธุรกิจและภาษีนิติบุคคล.

- กรมสรรพากร. (2568). หลักเกณฑ์และแนวปฏิบัติด้านภาษีเงินได้บุคคลธรรมดา.

- สยาม ลีเกิล อินเตอร์เนชันแนล. (2568). บริการให้คำปรึกษาด้านกฎหมายและภาษีสำหรับชาวต่างชาติในประเทศไทย.

ขอใช้บริการนักวิชาชีพของสมาคมได้ที่:https://www.seaproti.org/practitioners/

สมาคมวิชาชีพนักแปลและล่ามแห่งเอเชียตะวันออกเฉียงใต้ (SEAProTI) ได้ประกาศหลักเกณฑ์และคุณสมบัติของผู้ที่ขึ้นทะเบียนเป็น “นักแปลรับรอง (Certified Translators) และผู้รับรองการแปล (Translation Certification Providers) และล่ามรับรอง (Certified Interpreters)” ของสมาคม หมวดที่ 9 และหมวดที่ 10 ในราชกิจจานุเบกษา ของสำนักเลขาธิการคณะรัฐมนตรี ในสำนักนายกรัฐมนตรี แห่งราชอาณาจักรไทย ลงวันที่ 25 ก.ค. 2567 เล่มที่ 141 ตอนที่ 66 ง หน้า 100 อ่านฉบับเต็มได้ที่: นักแปลรับรอง ผู้รับรองการแปล และล่ามรับรอง

สำนักคณะกรรมการกฤษฎีกาเสนอให้ตราเป็นพระราชกฤษฎีกา โดยกำหนดให้นักแปลที่ขึ้นทะเบียน รวมถึงผู้รับรองการแปลจากสมาคมวิชาชีพหรือสถาบันสอนภาษาที่มีการอบรมและขึ้นทะเบียน สามารถรับรองคำแปลได้ (จดหมายถึงสมาคม SEAProTI ลงวันที่ 28 เม.ย. 2568)

สมาคมวิชาชีพนักแปลและล่ามแห่งเอเชียตะวันออกเฉียงใต้เป็นสมาคมวิชาชีพแห่งแรกและแห่งเดียวในประเทศไทยและภูมิภาคเอเชียตะวันออกเฉียงใต้ที่มีระบบรับรองนักแปลรับรอง ผู้รับรองการแปล และล่ามรับรอง

สำนักงานใหญ่: อาคารบ้านราชครู เลขที่ 33 ห้อง 402 ซอยพหลโยธิน 5 ถนนพหลโยธิน แขวงพญาไท เขตพญาไท กรุงเทพมหานคร 10400 ประเทศไทย